(440) 307-2060

(440) 307-2060

How Much Hail Damage Justifies a Roof Replacement?

When hailstones strike your roof, the damage varies dramatically based on size, roofing material, and impact location. In many cases, insurance will cover a full roof replacement—but first you need to know how size matters.

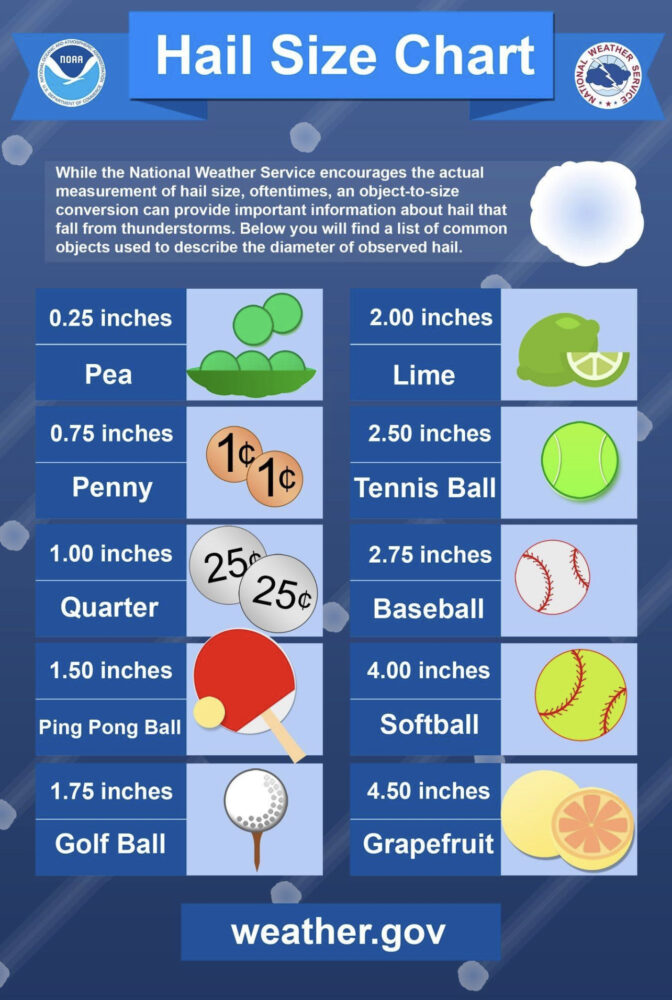

Visual Guide: Hail Sizes vs. Roof Damage 🎯

The image carousel above shows hail size chart comparisons:

- Pea-size (~¼″): Minimal impact—rarely causes damage.

- Penny / Marble-size (~¾–1″): Can cause bruises or granule loss.

- Quarter-size (~1–1¼″): Likely to crack or dent shingles.

- Golf ball (~1¾–2″+): Often fractures fiberglass mats—functional damage.

- Larger stones (2–3″ or more): Can severely damage shingles, fenestration, siding and gutters (Alpine Intel, superstormrestoration.com).

Asphalt shingles typically begin to sustain functional damage at 1″–1¼″ hail. Larger sizes significantly increase structural risk .

Recognizing Types of Hail Damage on Your Roof

- Granule loss: Visible in gutters and downspouts; exposes shingles to UV and moisture.

- Cracks or fractures: Especially on severe hail impacts; weakening the fiberglass mat layer.

- Bruising or indentations: Often accompanied by granule displacement around the impact.

- Damaged self-seal strips: Leads to shingles lifting or blowing off during high wind (Alpine Intel, superstormrestoration.com).

Even seemingly cosmetic damage, like granule loss or small cracks, can let in moisture and accelerate aging—insurers may deny purely cosmetic claims if functionality isn’t affected (insurance.com).

Impact-Resistant Shingle Classes: Picking the Right Protection

Class 1–3 Shingles

- Most standard asphalt shingles fall into Classes 1–3.

- They offer minimal hail resistance—sometimes cracking or shedding during moderate sized hail.

Class 4 Impact-Resistant Shingles

- Engineered to withstand severe hail: no visible fractures even after golf‑ball size impacts.

- Often made with SBS-modified asphalt or reinforced synthetic blends.

- Qualify for insurance discounts of 5–35% in many regions.

- Recommended if you live in hail-prone areas of Texas, Colorado, Kansas, etc. (Insurance Claim Recovery Support, glauserroofingsf.com).

U.S. Regions with the Most Hail Damage (“Hail Alley”)

Hail damage tends to concentrate in the Central U.S.—especially states in “Hail Alley.”

According to recent data:

- Nebraska (206 storms/year, $50.8M annual damage) topped the list

- Followed by Colorado ($151M), Texas ($338.6M), Kansas ($32.8M), Oklahoma ($80M), Iowa, Missouri, South Dakota, North Dakota, and Arkansas (foxweather.com, trailstoneinsurancegroup.com).

Major increases in severe hail events from 2022 to 2024:

- Missouri: +182%, 437 severe storms

- Illinois: +108%

- Indiana: +107% (including softball-sized hail)

- Texas: +93%

- Pennsylvania: +88%

- Kansas: +71%

- Colorado: +65% (Insurify).

Cities in Texas, Colorado, Nebraska, Oklahoma City, St. Louis, and Dallas regularly experience devastating hail damage requiring full replacements.

Hail size itself is growing too—climate change is increasing hail intensity, leading to insurers raising premiums and limiting coverage in affected regions (businessinsider.com).

Should You Replace Your Roof? Hail Damage Evaluation

Key hail size thresholds for damage:

- <¾″: mostly cosmetic, unlikely to require replacement.

- ~1″ (quarter-size)–1¼″: often causes cracks and granule loss. Requires inspection.

- ≥1½″ (golf-ball size or larger): very likely functional damage—replacement strongly recommended (Alpine Intel).

An experienced roofing inspector or contractor should evaluate:

- Extent and spread of impact marks

- Condition of granules and seal strips

- Roof age (older roofs may be covered less generously by insurers) (superstormrestoration.com, Investopedia).

Hail Damage Insurance Claim Process: Step-by-Step

1. Immediate Documentation & Notification

- Call your insurance provider as soon as possible. You’ll usually get a claim number and instructions.

- Take photos and video of damage—gutters, shingles, vents, etc.—as soon as it’s safe (insurance.com).

2. Temporary Repairs to Prevent Further Damage

- Tarps or boarding may be needed to avoid leaks. Keep all receipts.

- Document the condition before repairs for claims purposes (Insurance Claim Recovery Support).

3. Professional Inspection

- The insurer will send an adjuster to inspect the damage.

- You can have your roofing contractor attend to advocate for full coverage of hail damage and code upgrades—keeping documentation of everything (stormsurgeroofing.com).

4. Settlement & Repair

- Insurer delivers an estimate and settlement offer—often in two stages (initial and final) depending on work completed.

- If you disagree, you may negotiate or hire a public adjuster to advocate for you.

- Keep damaged materials and photos until final inspection is done (stormsurgeroofing.com, insurance.com, Insurance Claim Recovery Support).

5. Appealing a Denied Claim

- If adjuster says no damage, you can escalate the issue or hire a public adjuster.

- Documentation and contractor phoneline support are crucial for appeal success (insurance.com, Insurance Claim Recovery Support).

Timelines

- Most policies require notice within days and signed proof of loss within 30 days of request.

- Some states allow up to 1–2 years—but delay increases risk of denial due to assumption of neglect (Insurance Claim Recovery Support).

Choosing the Right Shingle After Hail: Focus on Class

If hail damage is confirmed, choosing a replacement product matters:

- Standard asphalt architectural shingles (Class 1–3): lower cost, limited hail resistance, more likely to crack under new storms.

- Class 4 impact-resistant shingles (e.g. UL 2218-certified): far more durable, withstand up to golf-ball hail stones without fail.

- These can offer insurance premium discounts up to 35% and long-term value for homeowners in hail-prone regions (CARE Public Adjusters).

Often, insurers cover upgraded Class 4 shingles if hail was severe, especially if the policyholder requests a stronger material for replacement.

Why Climate Trends & Insurance Costs Are Rising

- Insurance companies face mounting payout losses due to more frequent and larger hailstorms.

- Hail damage is becoming a bigger climate concern than wildfires or hurricanes for insurers (businessinsider.com).

- Many policies are now excluding cosmetic-only hail damage, increasing deductibles, or limiting coverage for older roofs (houstonchronicle.com).

Local Preparedness Tips (Especially for “Hail Alley”)

If you’re in states like Nebraska, Kansas, Texas, Colorado, Oklahoma, Missouri, Iowa, or South/North Dakota—here’s what to do:

- Review your homeowner’s insurance policy—check for hail exclusions or high deductibles.

- After hail, document damage quickly with time-stamped photos.

- Request an inspection by a licensed contractor experienced in hail claims.

- Opt for Class 4 shingles if replacement is needed—ask about insurance premium discounts.

- Stay proactive—outside hail season, keep your roof well maintained to prevent denial of claims due to neglect.

Summary Table: Hail Size, Damage & Recommended Action

| Hail Size | Typical Damage | Insurance Coverage? | Recommended Steps |

|---|---|---|---|

| <¾″ (pea/penny) | Cosmetic only; minor granule loss | Usually no | Monitor roof; document if frequent |

| ¾–1¼″ (quarter) | Potential cracking or bruising | Likely yes | Get inspection; file claim if granule loss or fractures |

| ≥1½″ (golf ball+) | Functional damage—fractured mat | Almost always yes | File claim; request Class 4 replacement |

Final Takeaways: Protecting Your Home & Wallet

- Hail as small as ¾″ can be cosmetic—but 1″ or larger may warrant a full roof claim.

- Class 4 impact-resistant shingles offer optimal defense and can reduce insurance costs.

- Living in “Hail Alley”? Keep policies updated, document storms, and choose experienced contractors.

- Insure quickly, advocate at inspections, and appeal if necessary—don’t settle until you’re confident the assessment is fair.

Hail damage roof replacement isn’t just about the roof—it’s about smart preparation, strong documentation, and choosing materials that resist the next storm.